Understanding Real Estate Valuation

Real estate valuation is a crucial aspect of the property market that determines the worth of a property based on various factors. This comprehensive guide delves into the methodologies, importance, and nuances of real estate valuation, particularly emphasizing the role of MAI certified appraisers in this complex field. Whether you are a seasoned investor, a homeowner, or just someone curious about how properties are valued, this article aims to elucidate the key concepts and practices involved in real estate valuation.

The Role of an MAI Certified Appraiser

Definition and Importance of MAI Certification

MAI stands for Member of the Appraisal Institute, a designation awarded to qualified appraisers who have completed rigorous education and experience requirements. This certification signifies a high level of expertise in real estate appraisal, particularly in the commercial sector. MAI certified appraisers are known for their deep understanding of market dynamics, advanced valuation theories, and ethical practices, making them invaluable in property transactions, litigation, and investment decision-making.

In the realm of real estate, selecting an appraiser with MAI certification can significantly impact the accuracy of property valuation. This designation ensures that the appraiser possesses a comprehensive set of skills, including the ability to analyze market trends and apply appropriate valuation methods, which ultimately leads to more informed decisions regarding investments and sales.

How an MAI Certified Appraiser Determines Property Value

MAI certified appraisers utilize a combination of methodologies to determine property value, including the sales comparison approach, cost approach, and income approach. The sales comparison approach evaluates similar properties that have recently sold, adjusting for differences in features or conditions. The cost approach estimates the value based on the cost to replace the property minus depreciation. The income approach, particularly relevant for investment properties, assesses the property’s potential to generate income, factoring in expenses and market conditions.

Each of these methods requires meticulous data collection and analysis to arrive at an accurate valuation. MAI certified appraisers also consider external economic factors, zoning laws, and property development trends to provide a holistic view of the property’s value. Their expertise ensures that valuations are not only accurate but also reflective of current market conditions.

Benefits of Hiring an MAI Certified Appraiser

Engaging an MAI certified appraiser offers numerous benefits, particularly in complex valuation scenarios. For investors, having a certified expert can mean the difference between making a sound investment or incurring losses. MAI appraisers bring a wealth of knowledge regarding the nuances of various property types and markets, which can be instrumental in making data-driven decisions.

Furthermore, MAI certified appraisers have a deep understanding of regulatory requirements and can navigate through the legal intricacies of property transactions, providing peace of mind to clients. Their ethical commitment ensures that the appraisal process is conducted with integrity, enhancing trust between all parties involved.

Determining Property Value

Factors Influencing Property Value

The value of a property is influenced by a myriad of factors, including its physical characteristics, location, market conditions, and economic factors. Physical characteristics such as size, condition, amenities, and age of the property play a significant role in its valuation. Additionally, features like landscaping, parking facilities, and energy efficiency can enhance or detract from a property’s appeal.

Location remains one of the most critical factors in property valuation. Properties situated in desirable neighborhoods with access to schools, shopping, and public transport typically command higher prices. Market conditions, including supply and demand dynamics, interest rates, and the overall economic environment, further influence property values. Understanding these elements is essential for anyone involved in real estate transactions.

Market Analysis and Comparable Sales

Market analysis is a fundamental component of property valuation, focusing on comparing similar properties within the same market. By examining recent sales data of comparable properties, appraisers can establish a benchmark for valuing a subject property. This comparative market analysis (CMA) involves evaluating factors such as sale prices, days on market, and unique features of comparable properties.

Through CMAs, appraisers can identify trends and fluctuations in the market that may affect property values. This analysis not only aids in setting realistic pricing but also helps stakeholders understand market dynamics and make informed decisions about buying or selling properties.

Role of Location in Property Valuation

Location is often referred to as the most crucial factor in real estate valuation. The adage location, location, location underscores its importance. Properties located in thriving urban areas or those close to amenities tend to appreciate faster than those in less desirable regions. The local economy, crime rates, school district quality, and community services also contribute significantly to a property’s value.

Additionally, zoning laws and future development plans can influence a location’s desirability. Areas slated for development may see increased interest and appreciation potential, while those facing economic decline may experience stagnant or falling property values. Understanding these location-related dynamics is vital for accurate property valuation and investment strategies.

Understanding Net Operating Income

Definition and Calculation of Net Operating Income

Net Operating Income (NOI) is a key metric in real estate investment, representing the income generated from a property after deducting operating expenses. It is calculated using the formula: NOI = Gross Rental Income – Operating Expenses. The gross rental income comprises all income received from rent and additional sources like parking fees or laundry services, while operating expenses include property management fees, maintenance costs, property taxes, and insurance.

A thorough understanding of NOI is essential for investors, as it directly impacts property valuation and investment yield. Accurate calculation of NOI requires diligent tracking of all income and expenses, ensuring that property owners have a clear picture of their net earnings from the investment.

Importance of Net Operating Income in Valuation

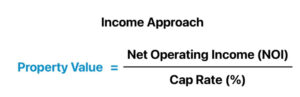

NOI plays a pivotal role in the valuation of income-producing properties, particularly when using the income approach. Investors and appraisers utilize NOI to estimate the property’s value by applying a capitalization rate, which reflects the expected return on investment in the current market. The formula used is: Property Value = NOI / Capitalization Rate.

Net operating income (NOI) is calculated by subtracting a property’s operating expenses from its total income. NOI is a measure of a property’s profitability.

This method allows investors to assess the potential profitability of a property and make comparisons against other investment opportunities. A higher NOI typically indicates a more profitable investment, thereby increasing the property’s overall value in the eyes of potential buyers or investors.

Common Mistakes in Calculating Net Operating Income

Calculating NOI may seem straightforward, but several common pitfalls can lead to inaccuracies. One frequent mistake is failing to account for all sources of income. Property owners may overlook additional income streams such as late fees or service charges, which can significantly impact the overall NOI.

Another error involves miscalculating operating expenses. For instance, excluding necessary costs such as maintenance reserves or utilities can result in an inflated NOI figure. To achieve an accurate calculation, property owners should conduct regular reviews of income and expenses, ensuring that all relevant factors are considered. This diligence not only promotes accurate valuations but also informs better decision-making regarding property management and investment strategies.

The Importance of Rent Roll

What is a Rent Roll?

A rent roll is a detailed report outlining all rental income generated by a property, including specifics about each tenant’s lease terms, rental amounts, and payment statuses. This document serves as a critical tool for property managers, investors, and appraisers in assessing the financial performance of an income-generating property.

In the context of property valuation, an up-to-date rent roll provides a snapshot of potential income streams, which is vital for determining the property’s overall value. Accurate rent rolls help in forecasting cash flows and enhance transparency in financial reporting, making them essential for effective property management.

How Rent Roll Affects Property Value

A well-maintained rent roll directly influences the perceived value of a property. Appraisers and investors rely on this document to assess the reliability and stability of income generated by the property. Properties with consistent rental income, long-term tenants, and low vacancy rates are typically valued higher than those with high turnover or unstable income streams.

If the rent roll reveals below-market rents or a high percentage of tenants on month-to-month leases, it may signal potential risks that could affect the property’s valuation negatively. Conversely, a strong rent roll indicating high demand and market rents can enhance the property’s attractiveness to potential buyers or investors.

Best Practices for Maintaining an Accurate Rent Roll

Maintaining an accurate rent roll requires regular updates and diligent record-keeping. Property managers should ensure that all lease agreements, renewals, and tenant changes are promptly documented to reflect current occupancy and rental rates. Using property management software can streamline this process, providing real-time access to rental income data and lease details.

Additionally, conducting regular audits of the rent roll helps identify discrepancies, ensuring that all financial information is accurate and reflective of the property’s current state. By prioritizing the integrity of the rent roll, property owners can make informed decisions about pricing, management, and future investment opportunities.

Financing Options: Hard Money and Private Investors

Definition of Hard Money Loans

Hard money loans are short-term financing options secured by real estate assets, typically used by investors seeking quick access to capital. Unlike traditional loans, hard money loans are based on the property’s value rather than the borrower’s creditworthiness. This makes them appealing for those looking to finance quick flips, renovations, or investment purchases without the lengthy approval process associated with conventional lending.

Typically offered by private lenders or investment firms, hard money loans usually come with higher interest rates and shorter terms compared to traditional mortgages. They can be an effective tool for investors needing immediate funding, but they also carry risks, as failure to repay can result in loss of the underlying asset.

Pros and Cons of Using Hard Money for Investment

The primary advantage of hard money loans is the speed of financing. Investors can close deals quickly, capitalizing on opportunities that require immediate action. Additionally, hard money lenders often have more flexible underwriting standards, which can benefit borrowers with less-than-perfect credit histories or unusual property types.

However, the downsides include higher interest rates and fees, which can significantly impact profitability. Moreover, the short repayment terms can create financial strain if the property does not sell or generate income quickly enough. Investors must carefully weigh the pros and cons of hard money financing in the context of their overall investment strategy.

Understanding Private Investors: Roles and Benefits

Private investors play a crucial role in real estate financing, providing capital for various projects without the constraints of traditional lenders. These investors can range from individuals to small investment groups and often seek a higher return on their investment compared to conventional savings or stock market options. Their involvement can take various forms, including equity partnerships, joint ventures, or direct financing for specific projects.

The benefits of engaging private investors include increased flexibility in financing terms and a more personalized approach to investment. Private investors may be more willing to fund unconventional projects or provide capital on terms that align better with the investor’s plans. However, it is essential to establish clear agreements and expectations to foster successful partnerships and mitigate potential conflicts.

Conclusion

Recap of Key Points

Understanding real estate valuation is vital for anyone involved in the property market, from homeowners to seasoned investors. Key components such as the role of MAI certified appraisers, the significance of Net Operating Income, and the impact of a well-maintained rent roll play crucial roles in determining property value. Additionally, exploring financing options, such as hard money loans and private investors, can open new avenues for investment opportunities.

Final Thoughts on Property Valuation and Investment

As the real estate market continues to evolve, staying informed about valuation practices and investment strategies is essential for success. By leveraging the expertise of certified professionals and understanding the intricacies of property valuation, investors can make informed decisions that maximize their returns and minimize risks. Continuing education and proactive management are key to thriving in this dynamic industry.

FAQs

What is the purpose of an MAI certified appraiser?

MAI (Member of the Appraisal Institute) certified appraisers provide expert property valuations that help buyers, sellers, and investors make informed decisions. They utilize advanced methodologies to assess property value accurately.

How does location affect property value?

Location significantly impacts property value due to factors such as neighborhood desirability, access to amenities, and economic conditions. Properties in well-regarded locations typically appreciate more than those in less desirable areas.

What is Net Operating Income, and why is it important?

Net Operating Income is a measure of a property’s profitability, calculated by subtracting operating expenses from gross rental income. It is crucial for assessing investment potential and value in income-producing properties.

What should be included in a rent roll?

A rent roll should include details such as tenant names, rental amounts, lease dates, payment statuses, and any additional income sources. This information is essential for accurately assessing a property’s income potential.

What are the risks associated with hard money loans?

Hard money loans come with higher interest rates and shorter repayment terms, posing risks such as financial strain if the property does not generate income quickly. Failure to repay can also lead to loss of the property.